Weekly: What Meta's cloud business might look like

14 min read.

Highlights

NYT on Intel, advanced packaging. Two longer pieces in the NYT: one on Intel’s recent efforts at a turnaround (resurgence of CPUs, inking major deals, opening new fab lines, a possible Terafab collaboration, mass layoffs) and another on the under-discussed industry of chip packaging, which is emerging as a new chokepoint in AI infrastructure development. Like AI chip manufacturing, TSMC dominates advanced packaging, while the lower-end chip packaging is primarily in Southeast Asia.

SemiAnalysis on Meta compute rental. SemiAnalysis offers a timely breakdown of what Meta’s compute rental business might look like, which might also apply to SoftBank’s freshly announced cloud business. SemiAnalysis is bullish that AI capex will continue this cropping of neocloud businesses is a sign of great demand for compute.

State of China’s EUV. Noah Tan, a junior fellow at Carnegie, writes in The Diplomat about China’s EUV progress. It is a follow up to news late last year the China had secretly built an EUV machine. While what China has now is more a research-use prototype, there is no consensus on when China might develop a proper EUV machine. Tan offers a state of where China is now - still lagging far behind industry standards regarding several EUV machine components.

Thanks for reading.

Table of Contents

Tripp Mickle, “Intel’s Chip Business Shows Signs of Life After Years of Struggle,” NYT, 06/26/2026.

Don Clark and Gabriela Bhaskar, “How a Niche Technology Became a Choke Point for A.I.,” NYT, 06/26/2026.

Richard Waters, “The chip rally is tightening tech’s grip on Wall Street,” FT, 07/03/2026.

Mike O’Brien, “Why Micron Is Betting Big on New York Chips,” WSJ, 06/30/2026.

Dan Gallagher, “The Long-Term Threat to the Memory Chip Boom Is Innovation,” WSJ, 06/26/2026.

Jeremie Eliahou Ontiveros, Max Kan, Joey Brookhart, et al., “Meta Compute: Everyone Wants To Be A Neocloud,” SemiAnalysis, 07/03/2026.

Noah Tan, “China’s EUV Lithography Progress: Parsing Signal From Noise,” The Diplomat, 07/02/2026.

1.

Tripp Mickle, “Intel’s Chip Business Shows Signs of Life After Years of Struggle,” NYT, 06/26/2026.

Not long ago, Intel, which was once one of the most powerful tech companies in the world, was described as Silicon Valley’s fallen icon. Sales were plummeting, costs soaring and debts mounting. The U.S. government intervened last summer and took a 10 percent stake in the company.

Now, Intel is showing signs of a turnaround. Its value has more than tripled to $650 billion, its business has started to rebound behind the artificial intelligence boom, and it has added big customers like Nvidia and Apple.

Tech giants were pouring hundreds of billions of dollars into chips for data centers. A.I. personal assistants known as agents — relying on chips called central processing units, or CPUs, Intel’s signature product — gained popularity. At the same time, Taiwan Semiconductor Manufacturing Company, which makes more than 90 percent of the world’s advanced semiconductors, was flooded with more orders than it could fill.

Intel, which opened a factory near Phoenix that uses new technologies to make denser, more energy-efficient chips, immediately began to benefit from the new dynamics. In September, Nvidia said it would invest $5 billion in Intel and use custom-made Intel CPUs in personal computers and data centers. Intel shares rose 23 percent on the news.

In May, Mr. Musk and Mr. Tan agreed that Intel would provide its technology to support a chip-making operation that Mr. Musk is developing called Terafab. And in recent months, Apple, which is among the world’s largest chip customers, agreed to begin manufacturing a small portion of its laptop chips at Intel’s factories as early as 2027, four people familiar with the confidential agreement said. Some smartphone chips may follow.

Each deal carries major caveats. In the agreement with Nvidia, each company will be selling the product, which means the amount of money that Intel makes on each chip can depend on who sells it, said three people close to the company, speaking on the condition of anonymity to discuss the confidential agreement.

The agreements with Mr. Musk and Apple hinge on Intel’s progress with a new manufacturing process it is developing called 14A. This fall, it has promised to deliver those companies a tool kit to test the technology before final commitments, one of the people close to Intel said.

In the face of that uncertainty, Mr. Tan has pushed the company to cut costs. It has reduced staff through layoffs and attrition to around 78,500 employees, from the 108,900 it had when he arrived. It wants to eventually be a 75,000-person company.

2.

Don Clark and Gabriela Bhaskar, “How a Niche Technology Became a Choke Point for A.I.,” NYT, 06/26/2026.

Subramanian Iyer, an electrical engineer and educator, has long specialized in a sleepy niche of the semiconductor industry that has now become a major choke point in the global contest for artificial intelligence leadership.

That niche is a technology called advanced chip packaging, which bundles as many as dozens of the components in palm-size modules. As computing gains from the traditional practice of shrinking transistors to pack more of them onto each chip have diminished, Nvidia and other chip giants have turned to packaging as an essential way to deliver semiconductors capable of more complex tasks for A.I.

Taiwan Semiconductor Manufacturing Company, which makes cutting-edge chips for Nvidia and other A.I. leaders, also packages nearly all of them. Its key suppliers and partners are mainly in Taiwan, too, facing the same threat from China that caused U.S. policymakers to funnel billions of dollars into boosting domestic chip fabrication.

The packaging bottleneck has become a hot topic in Silicon Valley as TSMC has struggled to keep up with demand. Dr. Iyer tried to help by developing plans for a packaging research and development center, funded with $1.1 billion from the Biden administration and slated to be built in Arizona, but the Trump administration effectively killed the effort last year.

The bottleneck underlines how U.S. dependence on Taiwan has not eased despite efforts by the Biden and Trump administrations. The Biden administration allocated more than $50 billion to jump-start domestic chip production under the 2022 CHIPS and Science Act. President Trump, objecting to grants to chip makers, has instead pressed for deals with U.S. companies that include equity stakes and threatened foreign companies with tariffs to essentially accomplish the same thing.

Amkor Technology, a packaging specialist, is building its first U.S. factory site in Arizona and is expected to take on some packaging work for TSMC under a 10-year deal. Amkor, which the Biden administration awarded a $407 million grant, boosted its own potential investment on the site to $7 billion after talks with Trump administration officials and signs of purchasing interest from Nvidia and Apple.

Packaging was long considered an afterthought that U.S. chip makers farmed out to countries in Asia with low wages. The U.S. share of chip packaging is around 3 percent, according to the Global Electronics Association.

3.

Richard Waters, “The chip rally is tightening tech’s grip on Wall Street,” FT, 07/03/2026.

Is this peak semiconductors? Memory, in particular, is a notoriously cyclical industry. After the Fomo that helped fuel the latest furious rally, the market experienced a predictable bout of nerves last week. But even if chip cycles aren’t forever, it’s hard to call an end to this one quite yet.

Predictably, this surge in demand has already prompted a huge increase in supply, both of planned chipmaking capacity and newly minted chip stocks. One sign is the $600bn that memory chipmakers Samsung and SK Hynix said this week they plan to invest in Korea. Another is the $29bn that SK Hynix hopes to raise when its American depositary receipts begin trading in the US next week.

Michael Burry, the short seller famous for predicting the subprime mortgage crisis, pointed to the Korean investment as a good reason for increasing his bet against AI. But with this new production capacity taking two or three years to come online, relief from the memory squeeze won’t come quickly.

Also, some of the biggest chip buyers are already looking past the next potential down cycle, suggesting its effects may be more muted. Micron said last week that it had agreed a number of long-term deals, including five-year supply contracts with some of its biggest customers that would put a floor under its prices when and if things turn down.

Further out, there are questions about whether the chip industry’s supply chain will be able to meet the growing demand. ASML, which makes machines essential to advanced chipmaking, and TSMC, which does most of the manufacturing, are potentially serious bottlenecks.

TSMC has said it will boost its capital spending by as much as 37 per cent this year, as it did in 2025. But those increases follow two years of retrenchment and would leave 2026 capex only around 50 per cent higher than 2022.

Contrast that with the biggest buyers of AI chips. Seven of the largest data centre operators are planning to spend an astounding $848bn this year, at least five times what they spent in 2022, according to a calculation by the newsletter Exponential View.

If the tech companies are right and demand for AI takes off from here, the chip squeeze looks far from over. But with semiconductor stocks running up so far, so fast, investors are still likely to find plenty to be anxious about.

4.

Mike O’Brien, “Why Micron Is Betting Big on New York Chips,” WSJ, 06/30/2026.

Your editorial “Chuck Schumer’s Chip Shortage” (June 23) raises concerns about permitting delays that I’ve seen first-hand.

After more than 30 years in the semiconductor industry, I served in the CHIPS Program Office under both the Biden and Trump administrations, working on more than a dozen semiconductor projects, including Micron’s. Leading-edge fabrication plants in Asia are built in half the time it takes in the U.S. But even Micron’s faster-permitted Boise, Idaho, fab won’t contribute meaningful DRAM supply until late 2027. The memory industry has always been cyclical, and today’s prices reflect an unprecedented global supply-demand imbalance.

There are reasons Micron chose New York. Over the years, IBM, GlobalFoundries, onsemi, Wolfspeed, Albany NanoTech, SUNY, NY CREATES, Empire State Development and CenterState CEO helped build one of America’s premier semiconductor clusters in the state. Gov. Kathy Hochul and the Legislature reinforced those advantages through the 2022 NY Green Chips Act, which led to up to $5.8 billion in incentives for the Micron project. Few states could compete with that.

Political leaders claim credit for projects, but no $100 billion site-selection decision turns on one official. Micron chose New York because project incentives were layered on decades of investment in a world-class semiconductor ecosystem—including available water, low-cost energy, research infrastructure and workforce development.

5.

Dan Gallagher, “The Long-Term Threat to the Memory Chip Boom Is Innovation,” WSJ, 06/26/2026.

Memory chip companies will have no problem selling everything they can make for a while. The biggest risk now is that their largest customers start getting creative.

Micron has also locked up long-term supply deals with 15 new customers, compared with only one such deal reported in the last quarter. Those discussions gave Micron enough visibility to project the shortage running beyond 2027, whereas the company had previously been keeping its comments about industry conditions limited to the current calendar year.

For the time being, all those companies are at the mercy of memory chip prices that keep moving higher. Apple even took the unusual step Thursday of raising prices for several of its products between launch cycles, citing memory costs. But necessity is also the mother of invention, and there are growing signs that the tech industry is hard at work on ways to reduce future dependence on the volatile component.

The prospect of technological breakthroughs that reduce future memory demand is worrisome for investors, given how much the market values of memory chip makers have soared over the past year. Micron alone lost nearly a third of its value in late March after Google published a research paper about TurboQuant, a compression algorithm that sharply reduced memory use without sacrificing AI model performance.

The harsh reality remains that anything that computes needs some form of system memory. And the largest consumers of that memory are worried enough about future supply to sign long-term agreements that would have once been unthinkable for a commodity with volatile prices. Micron said Wednesday that most of its latest deals are five years in duration and lock in price floors that will still be far better than those seen in past down cycles. “Even at floor prices, the contracts still beat past-cycle peak margins,” Futurum analyst Rolf Bulk said.

6.

Jeremie Eliahou Ontiveros, Max Kan, Joey Brookhart, et al., “Meta Compute: Everyone Wants To Be A Neocloud,” SemiAnalysis, 07/03/2026.

With Bloomberg headlines suggesting Meta could become a Neocloud, the market’s reaction was immediate: aggressive sell-off of Neoclouds like Coreweave & Nebius, and debates of “overcapacity” coming back. Let’s set the record straight – we believe that both takes are erroneous and that Meta’s datacenter & compute procurement will accelerate, not slow down. Capex in 2027 will be shockingly high. In just the first six months of the year, Meta has contracted over 5GW of capacity across Cloud & Colo, and that doesn’t even include all their accelerating self-build activity. Everything is computer and everything is a neocloud.

Meta’s capacity under construction just keeps accelerating. Of course, this naturally raises the questions of what Meta will do with this compute, and whether they’re going to flood the market with all of this supply if they turn into a Neocloud. Broadly speaking we see four major high-value use-cases, which are all differentied and very different relative to what traditional Neoclouds do:

Frontier AI Models: Meta has NOT given up on training frontier models. The bulk of incremental capacity still goes to Meta Superintelligence Labs, and we think the team is currently excited about their progress. A follow-up report will dive into MSL, their unique data strategy, and discuss their chances of catching up with Anthropic and OpenAI. Of course, our Tokenomics Model subscribers already know our takes and have access to all of this real-time.

RecSys: We believe Meta thinks they can scale up Ads recommendation systems by >10x in complexity to accelerate revenue growth. That requires both inference & training compute for their RecSys models. They can also do more generative targeted ads.

(SemiAnalysis Exclusive) We believe that Meta is in final talks with Anthropic to get access to private instances of Claude. This would be akin to Bedrock, Foundry, Vertex from other hyperscalers (read our deep dive here). There are multiple use-cases for Meta, ranging from internal usage, to building the premier Sales & Marketing SaaS powered by Frontier AI Agents. We expect Meta to launch a token-as-a-service endpoint and increasingly move up the stack, leveraging its network and distribution. Initially it will be their own models externally and Anthropic internaly, but over time we believe they will serve Anthropic and OpenAI models externally

We expect Meta to strike a few “SpaceX-type” deals. Elon is a sales genius, and he created a brand new market segment: large-scale on-demand compute at a huge pricing premium. We think Meta wants in, but selectively. After all, just a couple hundred MWs can already drive >$10B of yearly revenue! We expect a ten billion dollar Anthropic deal to kick off the flywheel.

This high optionality, with four high-value-add options, makes it easy for Meta to keep aggressively contracting compute. Meta Superintelligence remains the core engine, but if it doesn’t work out, there are many high-margin alternatives to sell compute. It is essentially a CFO’s dream and makes it very easy to go all-in on compute – we bet Susan did a 180° flip when she saw the pricing of SpaceX compute deals! Meta won’t be a normal bare-metal IaaS vendor with ~30% gross margins – all its options are high value, and enable to easily afford paying a margin to other Neoclouds in order to accelerate their fleet buildout - even if MSL doesn’t work out.

7.

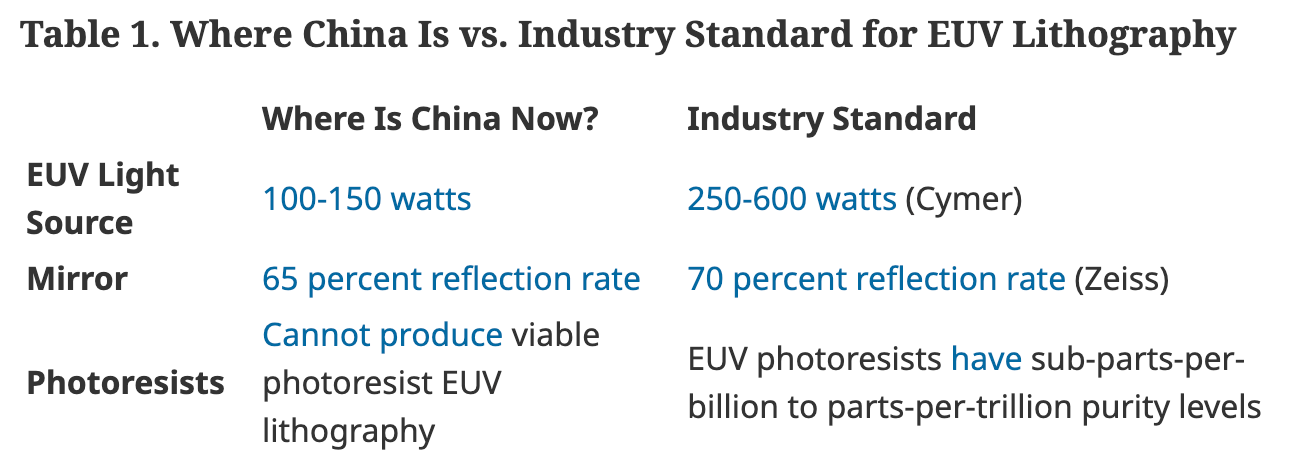

Noah Tan, “China’s EUV Lithography Progress: Parsing Signal From Noise,” The Diplomat, 07/02/2026.

When Reuters reported in December 2025 that researchers in Shenzhen had secretly built a prototype for an extreme ultraviolet (EUV) lithography machine, an indispensable piece of equipment for producing the most advanced chips, commentators debated when China will be able to overcome one of the last remaining obstacles to manufacturing its own advanced semiconductors.

Whether this prototype is a near-term inflection point or a mere steppingstone on a long journey remains difficult to predict. Chinese insiders claim that 2030 is a “realistic target” for making working chips from its prototype, while skeptics posit that it will take decades to reach commercial viability.

There is a way to cut through the noise. Building an EUV machine depends on specific technical chokepoints that can be identified and monitored. Three of the most important are developing high-power, ultra-low-wavelength light sources that print the circuit patterns; creating incredibly smooth mirrors that reflect EUV light onto silicon wafers with atomic-scale precision; and producing the ultra-pure, light-sensitive photoresist chemicals which convert the light blueprint into a physical stencil for the chip’s microscopic wires.

China’s timeline toward an EUV machine is uncertain, but tracking these specific areas can help analysts and policymakers gauge how close Beijing is to semiconductor self-reliance.

Policymakers, scholars, and industry analysts have not reached a consensus on China’s timeline toward a domestic EUV machine. Estimates range from a few years to several decades.

–